By Warrior’s Heart Enterprises LLC | Featuring Jason D. Murry, Lead Agent – Kintsugi Financial Leadership

There’s an old Japanese art called Kintsugi — the practice of repairing broken pottery with gold, making the once-broken piece more valuable than it was before. The cracks aren’t hidden… they’re honored. Restored. Strengthened.

That same principle guides the work of Jason D. Murry — a devoted husband, father, ordained chaplain, martial arts instructor, and the founder of Kintsugi Financial Leadership, a division of Warrior’s Heart Enterprises LLC, in alliance with Experior Financial Group, Global View Capital, and Quantum/Annexus.

Jason didn’t come from financial royalty. In fact, his journey started from the financial trenches — a fractured background filled with scarcity, fear, and dysfunction. But just like the warrior disciplines he teaches in Karate, Jason turned that pain into purpose.

Now, his life’s mission is helping others do the same — especially those who’ve been told they’re too late, too broken, or too behind.

The True Account of the Widow’s Jar: What You Think Isn’t Enough Is Often Just the Beginning

There was a widow in 2 Kings 4 who was drowning in debt. Creditors were coming to take her sons as payment. All she had was a small jar of oil. But God multiplied what she had when she obeyed in faith.

Jason and his team met a single mother who felt exactly like that widow — financially cornered, fearful, but willing to try. She only had $68 per month of room in her budget. But through the Expert Financial Analysis (EFA), Jason and his team showed her how to secure a $650,000 Term Life Policy with Living Benefits — a policy designed to not just protect her son if she passed away, but also cover her during her lifetime in the event of chronic, critical, or terminal illness.

The woman was relieved and emotional when she saw the approval. Not because of cost — but because for the first time, someone made it possible that she could her son a legacy in case she were to pass.

The Parable of the Unwise Steward: Don’t Let Time Work Against You

Jesus once told a story about a servant who mismanaged what was entrusted to him, failing to prepare for the future (Luke 16). In the financial world, many families are told they have “coverage,” but don’t know what they’re covered with — or how dangerous that coverage may be as they age.

One such example? A 67-year-old gentleman came to Jason with a $300,000 Term Life Insurance policy. No living benefits. And worse — it was a Decreasing Term with an Annual Renewable Rider, meaning that as he aged, he’d pay more and get less. By 95 years old, he would be paying over $4,100 per month for just $150,000 in death benefit. A trap in plain sight.

Jason and his team secured him a new 10-year Level Term with Living Benefits and Conversion Option — locking in $300,000 of real protection for just $191/month.

The Parable of the Wise Builder: Dig Deep and Lay a Better Foundation

In Matthew 7, Jesus warns about those who build houses on sand — they may look stable for a while, but storms will reveal what’s underneath. A wise man builds on rock.

That’s exactly what a couple in their 50s chose to do when they reached out. Drowning in debt, burdened by minimum payments, and years away from freedom — they didn’t need a quick fix. They needed a new foundation.

Through DebtMedic, a strategic partner in Jason’s ecosystem, the Kintsugi team helped consolidate their obligations, cut their payments in half, and slashed years off their debt timeline — putting thousands back in their pocket and redirecting those dollars toward building wealth.

Real Talk: Stop Surviving. Start Building.

If you’ve ever thought:

“I’m tired of living paycheck to paycheck.”

“I want to break my family’s financial curses.”

“I need clarity. I need peace.”

Then hear this: You are not alone. And your past doesn’t disqualify you — in fact, it just might prepare you.

Whether you’re a single parent, a senior citizen, or a middle-class family with silent stress behind your smile or a high net-worth individual looking to expand their legacy further… there’s a team that’s fought this battle before and built a better way.

With a biblical mindset, a battle-tested team, and custom strategies that fit your real life, Jason D. Murry and Kintsugi Financial Leadership are here to help you build a durable financial legacy — not a temporary fix.

Take the First Step. It’s Free — But Powerful.

Book your customizable, complimentary Expert Financial Analysis (EFA) — and let’s have a real conversation about your finances, your goals, and how we can help you walk in peace, purpose, and financial clarity.

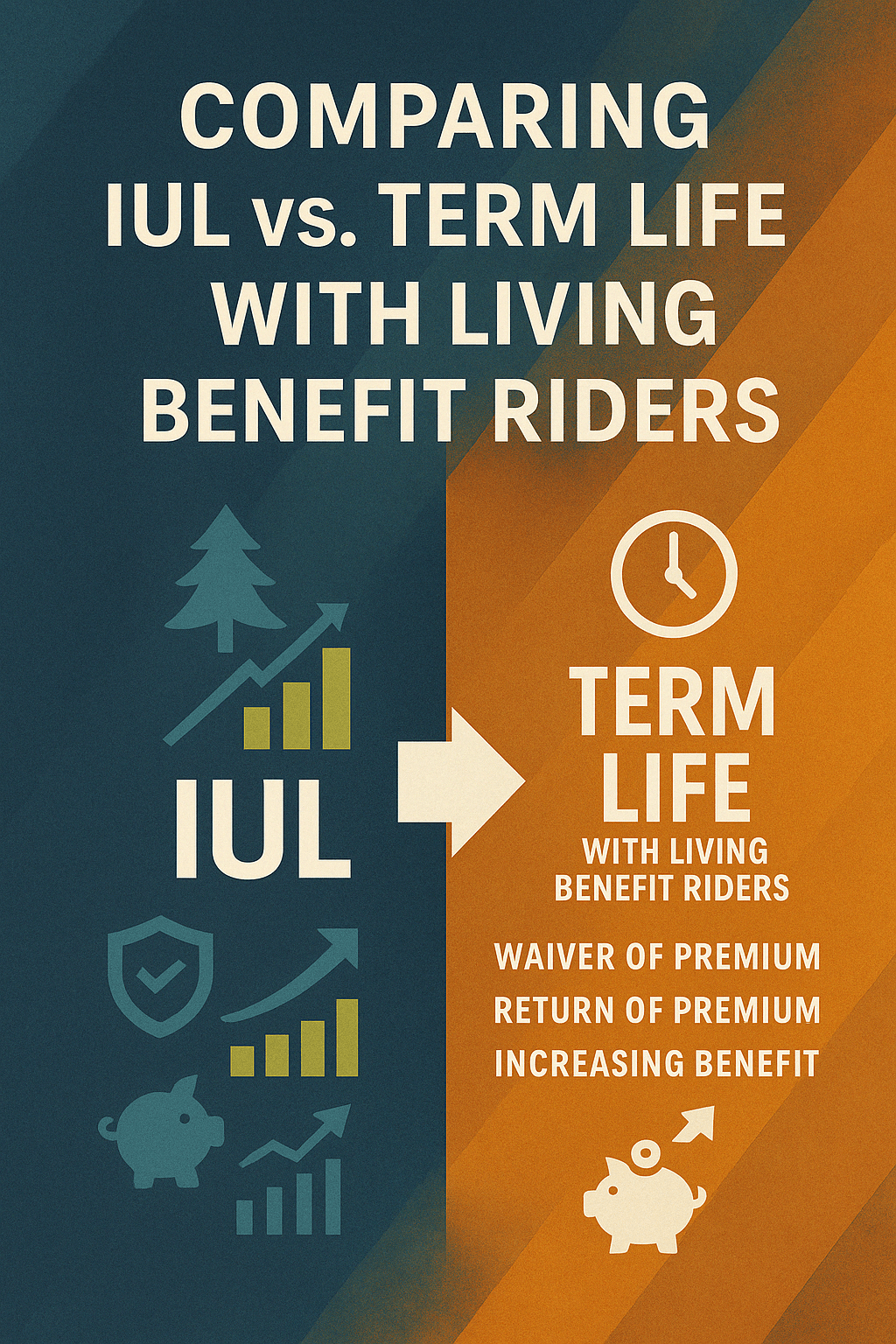

In the world of life insurance, choosing the right policy is crucial in protecting your loved ones and aligning your financial goals. Two popular approaches are Indexed Universal Life (IUL) insurance and Term Life insurance with Living Benefit Riders. This article examines these options while incorporating valuable riders such as waiver of premium, return of premium, and increasing benefit riders. We’ll also discuss how investing the savings from a term policy into a retirement Fixed Indexed Annuity (FIA) can be an effective strategy for long-term wealth accumulation.

1. Understanding the Basics

Indexed Universal Life (IUL) Insurance

IUL is a permanent life insurance policy that offers lifelong coverage. A portion of your premium goes toward building a cash value that increases based on a specific stock market index (such as the S&P 500) while protecting your principal from market downturns. The policy also provides flexibility in premium payments and death benefits. This dual functionality means you gain both a death benefit and an investment component, allowing tax-advantaged growth over time.

Term Life Insurance with Living Benefit Riders

Term life insurance provides coverage for a set period—typically 10, 20, or 30 years—at a lower cost. While it offers no cash value accumulation, it can be enhanced with living benefit riders. These riders enable you to access a portion of the death benefit in the event of a critical, chronic, or terminal illness, thereby providing financial relief while still alive. Living benefits are especially valuable for policyholders facing unexpected health challenges.

2. Enhanced Protection with Living Benefit Riders

Riders can significantly alter the risk and reward profile of your life insurance policy. Here, we discuss three key riders:

a. Waiver of Premium Rider

The waiver of premium rider protects you by suspending premium payments if you become totally disabled. This ensures that your policy remains active regardless of your inability to pay due to a disability. It relieves financial pressure during challenging times and guarantees that your coverage endures.

b. Return of Premium Rider

A return of premium rider offers an attractive proposition: if you outlive the policy term, you receive all or a portion of the premiums paid back at the end of the policy term. Although this rider usually comes at a higher cost, it adds a savings or cash-back component to what is otherwise a temporary safety net.

c. Increasing Benefit Rider

An increasing benefit rider allows the death benefit to grow over time to address the challenges of inflation and increased future financial needs. This rider ensures that the value of the protection you’re purchasing does not diminish in real terms over the long term. However, an increasing benefit rider typically leads to higher premiums as the risk to the insurer grows.

3. The “Buy Term and Invest the Difference” Strategy

For those who are cost-conscious yet seek robust retirement planning, the “Buy Term and Invest the Difference” strategy is worth considering.

Term Life Insurance as a Base

Term life insurance is far less expensive than IUL, allowing you to secure a significant amount of coverage at a lower cost. This affordability factor means that a larger portion of your income can remain available for other investments.

Investing the Difference into a Fixed Indexed Annuity (FIA)

A Fixed Indexed Annuity (FIA) offers a compelling retirement strategy. FIAs are designed to provide tax-deferred growth linked to market indices, with a guarantee against market losses through a guaranteed minimum interest rate or floor. Essentially, after paying for term insurance, the money saved can be directed into an FIA, which not only adds the potential for market-linked growth but can also provide a guaranteed stream of income during retirement. This approach divorces the investment component from the life insurance product, allowing each to perform in its optimal role.

4. Comparing and Contrasting the Two Approaches

IUL Insurance

Coverage Duration:

Lifelong protection under one policy.

Cash Value Component:

Accumulates cash value with potential tax-free access, but returns are subject to caps and participation rates.

Premium Flexibility:

Allows adjustable premiums and death benefits, though optimal performance requires ongoing funding.

Living Benefits:

Some IUL policies may offer limited living benefits; however, their core strength lies in the combined investment and insurance product.

Cost Considerations:

Higher premiums due to permanent coverage and cash value features.

Term Life Insurance with Living Benefit Riders + FIA Strategy

Coverage Duration:

Term coverage offers protection for a specific period, ideal for covering temporary obligations.

Cost Efficiency:

Lower premiums free up capital to invest.

Enhanced Riders:

Living benefit riders (waiver of premium, return of premium, and increasing benefit riders) enhance coverage during emergencies.

Investment Opportunity:

The savings from lower term premiums can be effectively invested into an FIA, which offers market-indexed growth with downside protection and potential retirement income.

Flexibility:

Conversion options may be available, allowing you to transition to permanent coverage as your needs evolve.

5. Which Option Fits Your Financial Goals?

The choice between IUL and a Term Life policy (enhanced with riders and coupled with an FIA investment strategy) depends on your priorities:

Opt for IUL if:

You desire lifelong protection with a built-in cash value component.

You are comfortable managing a more complex product with flexible but potentially higher premiums.

Tax-advantaged cash accumulation that can supplement retirement income is a key goal.

Opt for Term Life with Living Benefit Riders + FIA if:

You have a limited budget yet need significant coverage for your family’s immediate financial responsibilities.

You prefer to minimize your insurance cost while directing the savings to build retirement wealth.

You value supplemental riders that offer additional financial protection during health crises, along with the flexibility to convert if your circumstances change.

Conclusion

Life insurance is far from a one-size-fits-all product. An IUL provides lifetime coverage with investment benefits built into the policy but comes at a higher premium and greater complexity. In contrast, Term Life Insurance—when enhanced with riders such as waiver of premium, return of premium, and increasing benefit features—offers robust protection at a lower cost. When you invest the premium savings into a Fixed Indexed Annuity (FIA), you not only secure coverage for your family but also build a retirement nest egg that grows with market exposure while safeguarding your principal.

Ultimately, making an informed decision requires aligning your policy with your long-term financial objectives and risk tolerance. Consulting with Jason Murry & his financial strategists and advisors today! It is essential to tailor these strategies to your individual needs through our Expert Financial Analysis.

Increasing Benefit Rider: (While a dedicated Investopedia article may not exist solely for this rider, similar concepts are discussed in various insurance resources; you might start here for an overview on related topics and riders:) Investopedia – Understanding Term Life Insurance Riders

The Rule of 72: A Simple Yet Powerful Tool for Financial Growth

The Rule of 72 is a straightforward financial principle that provides a quick estimate of how long it will take for an investment to double in value, given a fixed annual rate of return. By dividing 72 by the annual interest rate, investors can approximate the number of years required for their investment to grow twofold.

For example, with an 8% annual return, the calculation would be 72 ÷ 8 = 9 years for the investment to double.

Why the Rule of 72 Matters

1. Simplifying Complex Calculations

The Rule of 72 offers a simple method to understand the effects of compound interest without delving into complex formulas. This makes it an accessible tool for both clients and financial professionals when making informed decisions.

2. Assessing Investment Growth

By applying this rule, investors can set realistic expectations for their investment horizons. It aids in comparing different investment opportunities and understanding how varying interest rates impact long-term financial goals.

3. Highlighting the Impact of Fees and Inflation

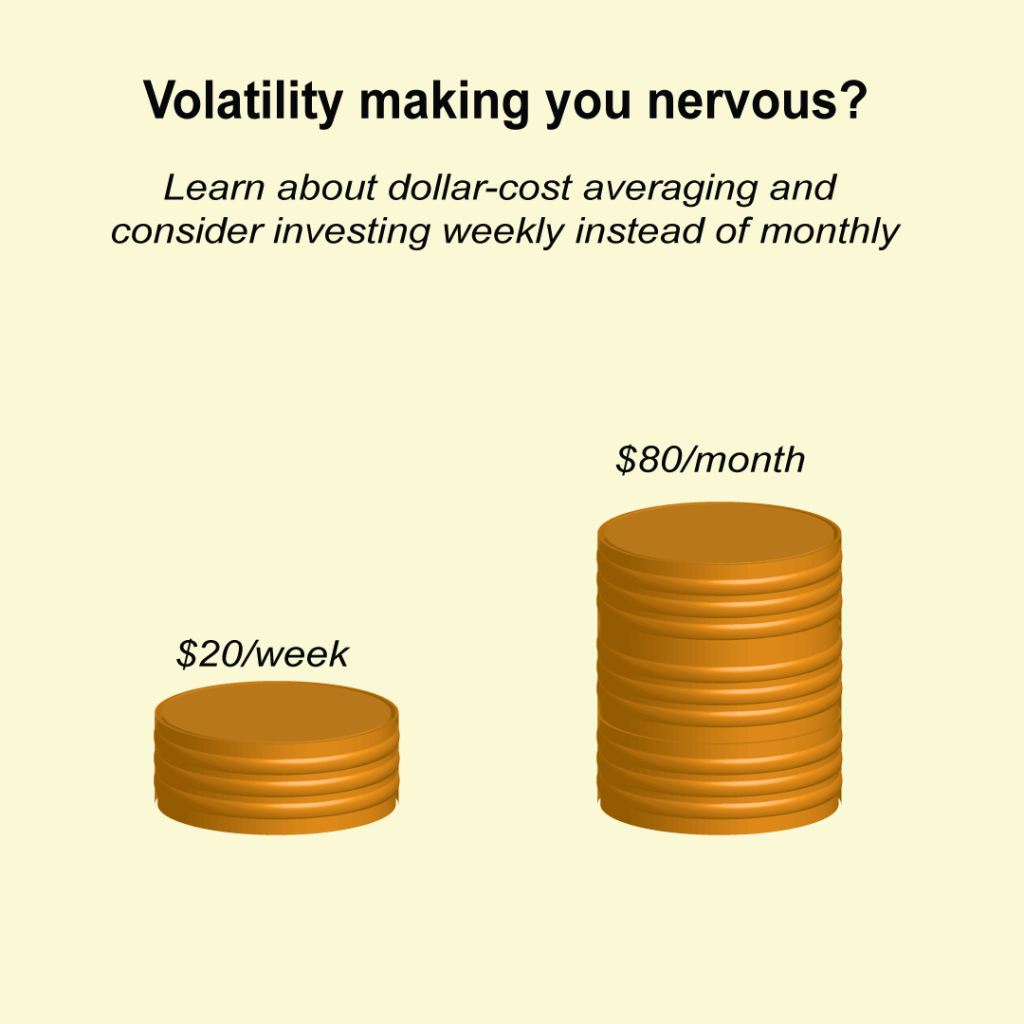

The Rule of 72 can illustrate how fees and inflation affect investment growth. For instance, an 8% return reduced by a 2% fee results in a net 6% return, extending the doubling time from 9 to 12 years. This underscores the importance of minimizing costs and accounting for inflation in financial planning.

Applications Beyond Investments

While commonly used for investments, the Rule of 72 has broader applications:

Understanding Inflation: Helps estimate how long it will take for the purchasing power of money to halve due to inflation. For example, at a 3% inflation rate, prices double approximately every 24 years (72 ÷ 3).

Debt Management: Highlights the long-term impact of high-interest debt, encouraging clients to make smarter borrowing decisions.

Limitations to Consider

While the Rule of 72 is a powerful tool, it’s important to recognize its limitations:

It’s an estimate, not an exact figure.

It assumes a constant interest rate, which may not reflect market volatility.

It presumes annual compounding, whereas different compounding periods may affect the results.

How Jason D. Murry and Kintsugi Financial Leadership Can Help

At Kintsugi Financial Leadership, Jason D. Murry and his team specialize in helping families, business leaders, and their businesses take full advantage of the Rule of 72 when investing for their financial futures and legacies. Whether you’re planning for retirement, growing your business wealth, or securing a lasting legacy, we provide strategic insights and tailored financial solutions to make your money work for you.

📞 Contact us today for a consultation intake and take the next step in building your financial future!

Schedule Consultation Intake Jason D Murry Founder/Owner Kintsugi Financial Leadership (918) 604-6434 teamwarriorsheart@gmail.com

How Many North Americans Experience Financial Vulnerability:

The financial landscape in America today paints a picture of growing uncertainty and vulnerability for many. Amidst the backdrop of a global pandemic, economic shifts have led to significant job layoffs, leaving countless individuals and families grappling with the immediate loss of income and the looming fear of what the future holds. This instability is compounded by concerns over the sustainability of social security, with projections suggesting that funds may be depleted by 2035. Such uncertainties underscore the critical need for comprehensive financial planning and literacy.

Moreover, the specter of high inflation has cast a long shadow over the cost of living, affecting everything from grocery bills to housing costs. This inflationary pressure, coupled with wages that have largely remained stagnant, has pushed an alarming 70% of American families into a cycle of living paycheck to paycheck since 2021. The immediate consequence of this financial precarity is not just the struggle to meet day-to-day expenses but also the inability to save for future needs or emergencies, leaving many just one unexpected expense away from financial crisis.

These challenges highlight the urgency of enhancing financial literacy and planning among Americans. Understanding how to navigate these turbulent financial waters is more than just a matter of personal security; it’s about building a foundation for future stability and prosperity. By focusing on financial education and leveraging innovative financial tools, individuals can gain the knowledge and confidence needed to make informed decisions about their financial futures. This is where the importance of accessible, clear, and empathetic financial advice becomes paramount, setting the stage for a journey toward financial empowerment and resilience.

An In-Depth Example of Living Paycheck to Paycheck:

Living paycheck to paycheck has become an all-too-common reality for a significant portion of Americans, a situation where individuals and families find themselves with just enough income to cover their monthly expenses, leaving little to no room for savings or unexpected costs. This financial tightrope walk is primarily driven by a combination of stagnant wages and the rising cost of living, exacerbated by persistent inflation. As prices for essentials like housing, healthcare, and groceries increase, salaries have not kept pace, forcing many to allocate a larger portion of their income to meet these basic needs.

The impact of inflation on everyday expenses cannot be overstated. It chips away at purchasing power, meaning that even if nominal wage increases occur, they may not be sufficient to keep up with the cost of living. This scenario places additional strain on already stretched budgets, making it difficult to set aside funds for emergencies or future financial goals. In such an environment, the absence of a financial buffer can lead to a cycle of debt, as people may resort to credit cards or loans to cover unexpected expenses, further exacerbating their financial precarity.

However, there are strategies to mitigate the effects of living paycheck to paycheck. Effective budgeting is the first step, requiring a clear understanding of income and expenses to identify areas where costs can be reduced. Creating an emergency fund, even with small, regular contributions, can provide a safety net for unforeseen expenses, reducing the need to incur debt. Additionally, leveraging financial tools and resources can offer insights into managing finances more effectively. For instance, Experior’s innovative tools, like FiN, can help individuals understand their financial situation better and make informed decisions about saving, spending, and investing.

While the challenges of living paycheck to paycheck are significant, they are not insurmountable. With the right approach to budgeting, savings, and the use of financial planning tools, individuals can create a buffer against financial instability, paving the way towards greater financial security and independence. It’s about making informed choices and taking proactive steps to manage one’s financial health, even in the face of economic uncertainties.

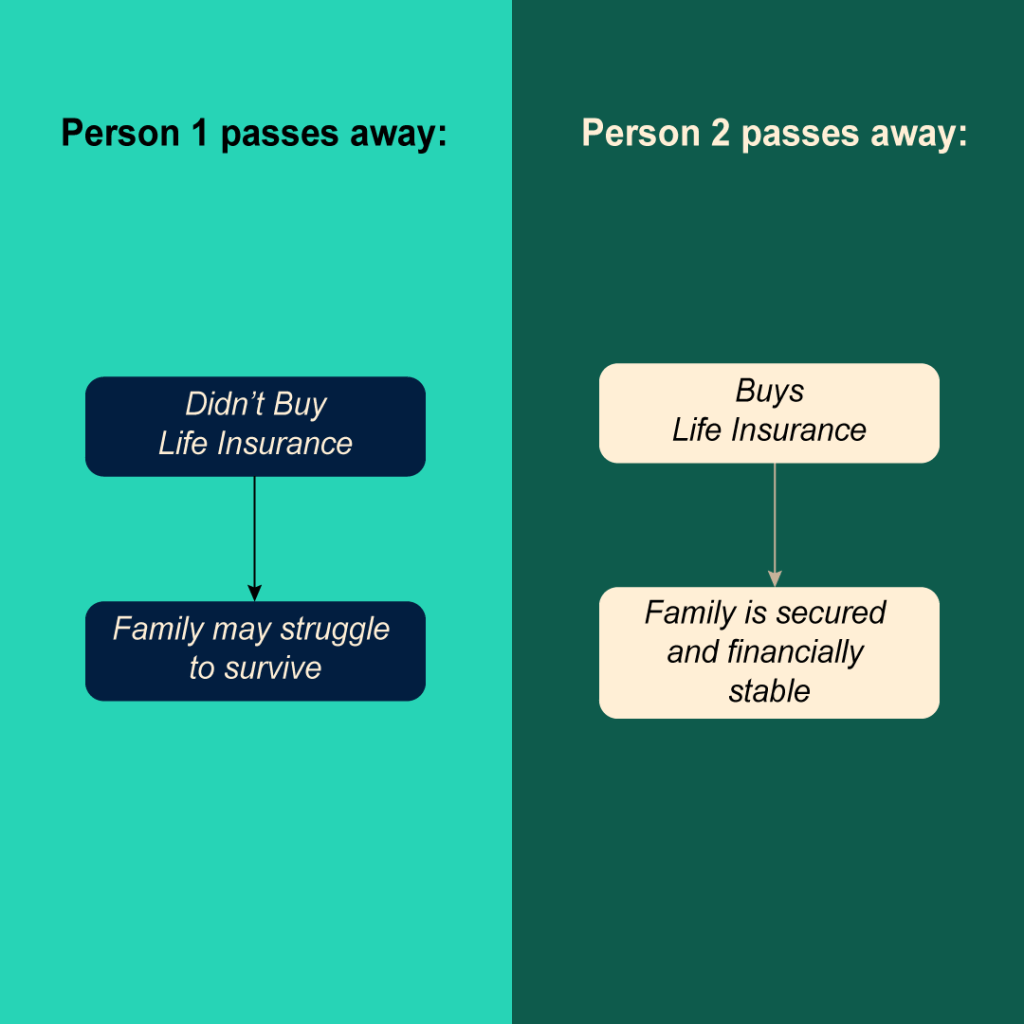

The Life Insurance Gap: The Risk:

Life insurance often gets overlooked in financial planning discussions, yet it plays a pivotal role in securing the financial future of families. It’s designed to provide a safety net, ensuring that in the event of an unexpected loss, the financial well-being of loved ones is preserved. Despite its importance, a significant portion of Americans remain underinsured or without any life insurance coverage at all. This gap in coverage can lead to devastating financial consequences, leaving families struggling to cope with expenses like mortgages, education costs, and daily living expenses in the absence of the deceased’s income.

There are several types of life insurance, each catering to different needs and life stages. Term life insurance, for instance, offers coverage for a specified period and is often a cost-effective option for young families. On the other hand, whole life insurance provides lifelong coverage along with a cash value component, which can be a valuable asset for long-term financial planning. Despite the variety of options available, many Americans shy away from purchasing life insurance due to misconceptions about its cost and the complexity of obtaining coverage. However, with the right guidance, finding a policy that fits one’s needs and budget can be straightforward and accessible.

Addressing common misconceptions is crucial in closing the life insurance gap. Many believe that life insurance is too expensive, yet the reality is that coverage can be quite affordable, especially for term life policies. Another barrier is the perception that the application process is cumbersome and time-consuming. Advances in technology have streamlined this process, making it easier than ever to apply for and obtain life insurance. By demystifying these aspects and highlighting the critical role of life insurance in a comprehensive financial plan, individuals can be encouraged to evaluate their coverage needs proactively.

Understanding one’s life insurance needs is a personal process and requires consideration of various factors, including financial obligations, dependents, and future goals. Tools like Experior’s innovative financial planning platforms can assist in this evaluation, providing insights and recommendations tailored to individual circumstances. By leveraging such resources, individuals can make informed decisions about the type and amount of life insurance that best suits their needs, ensuring their loved ones are protected against financial hardship in the face of life’s uncertainties.

In conclusion, life insurance is an essential component of a robust financial plan, offering peace of mind and security for the future. By educating individuals about the types of life insurance available, addressing misconceptions, and providing tools for evaluating coverage needs, we can bridge the gap in life insurance coverage and ensure that more families are protected against the financial impact of unexpected loss.

Retirement Planning in Uncertain Times:

Navigating the path to retirement has become increasingly complex, especially with growing concerns that social security funds might be insufficient in the near future. Coupled with the fact that many Americans are outliving their savings and 401(k)s, the need for strategic retirement planning has never been more critical. Assessing retirement readiness involves a thorough evaluation of current savings, projected expenses, and expected income sources in retirement. It’s about understanding not just how much you have saved, but also how long those savings will last given your lifestyle and the rising costs of healthcare and living expenses.

Diversifying retirement income sources is a key strategy in building a more secure financial future. Beyond traditional savings and social security benefits, exploring other income streams such as investments, annuities, or even part-time work in retirement can provide additional financial cushioning. This diversification helps mitigate risks, such as market volatility or longer-than-expected lifespans, ensuring that you have a steady flow of income throughout your retirement years.

Innovative tools, like FiN, offer valuable assistance in this planning process. FiN can help individuals understand their current financial situation, project future needs, and identify potential gaps in their retirement planning. By providing insights into various income sources and how they can be optimized for retirement, these tools empower users to make informed decisions that align with their long-term goals. Moreover, they encourage a proactive approach to retirement planning, highlighting the importance of starting early and adjusting plans as circumstances change.

In the face of uncertainties surrounding social security and the adequacy of savings, taking control of your retirement planning is essential. It’s about looking beyond the immediate horizon and laying the groundwork for a future that is both financially secure and aligned with your personal aspirations. With the right knowledge and tools, such as those offered by J. Murry Financial through Experior, individuals can navigate the complexities of retirement planning with confidence, ensuring they are well-prepared to enjoy their retirement years to the fullest.

The journey to a sustainable retirement requires both foresight and adaptability. By assessing retirement readiness, diversifying income sources, and leveraging advanced financial planning tools, individuals can build a retirement plan that not only withstands the test of time but also provides peace of mind. In an era marked by financial uncertainties, such preparedness is invaluable, offering a path to retirement that is both achievable and rewarding.

The Side Hustle Solution:

In today’s economic climate, where the cost of living continues to rise and traditional employment often falls short of covering all financial needs, exploring additional income streams has become a necessity for many. Side hustles, or secondary forms of employment taken on in addition to full-time jobs, offer a practical solution. They not only provide an extra layer of financial security but also present an opportunity for individuals to pursue passions or interests that may not be fulfilled in their primary careers. From freelance writing and graphic design to driving for ride-share companies or selling handmade goods online, the possibilities for side hustles are as diverse as the individuals pursuing them.

However, embarking on a side hustle comes with its own set of challenges. Time management, for instance, becomes crucial as individuals must juggle the responsibilities of their full-time job with the demands of their secondary employment. There’s also the risk of burnout, as dedicating additional hours to work can lead to stress and fatigue. To mitigate these challenges, it’s important to choose a side hustle that aligns with personal interests or skills, as this can make the extra work feel less burdensome and more like a fulfilling endeavor. Setting clear boundaries and dedicating specific times for the side hustle can also help maintain a healthy work-life balance.

For those considering a side hustle, the key is to start small and scale up gradually. This approach allows for learning and adjustment without overwhelming the individual. It’s also beneficial to leverage online platforms and social media to market the side hustle, reaching a wider audience without significant upfront costs. As the side hustle grows, it can become a significant source of income, offering not just financial stability but also the potential for full-time entrepreneurship.

In conclusion, side hustles represent a viable option for financial empowerment, allowing individuals to supplement their income and pursue their passions. With careful planning and dedication, a side hustle can transform from a simple means to make ends meet into a fulfilling career path. For those navigating the complexities of the modern financial landscape, considering a side hustle could be the key to achieving both economic stability and personal satisfaction.

What Now? I’m Glad You Asked:

The journey toward financial stability and empowerment is both necessary and achievable. As we’ve explored, the challenges of living paycheck to paycheck, the critical importance of life insurance, the complexities of retirement planning, and the potential of side hustles offer significant opportunities for individuals to enhance their financial literacy and take control of their future. Each of these areas, while distinct, shares a common thread: the need for proactive planning and the value of informed decision-making.

Empowering yourself financially means understanding the landscape, recognizing the risks, and taking steps to mitigate those risks. It’s about making choices today that will secure your tomorrow. This could mean reassessing your life insurance coverage to ensure your family’s future is protected, diversifying your income sources to build a more resilient financial foundation, or leveraging advanced tools to plan for a retirement that’s not just sustainable but also fulfilling.

Remember, you’re not alone in this journey. At J Murry Financial, we’re committed to providing personalized advice and support, helping you navigate the complexities of the financial world with confidence. Our partnership with Experior Financial Group & Global View Capitol Advisors equips us with innovative tools and resources designed to offer insights and solutions tailored to your unique situation. Whether you’re looking to better understand your financial health, explore insurance options, or plan for retirement, we’re here to help.

We invite you to take the next step toward financial empowerment. Reach out to us for a conversation about how we can support your goals and help you build a stronger, more secure financial future. Together, we can turn challenges into opportunities and aspirations into achievements.

Introduction to Financial Challenges Facing Families

In recent times, families across the nation have found themselves navigating a complex financial landscape marked by challenges both old and new. The once-reliable security of pensions has largely faded into memory, and the future of Social Security remains clouded with uncertainty. At the same time, advances in healthcare have led to longer life expectancies, which, while a cause for celebration, also introduce new considerations for retirement planning. These factors, compounded by the ever-present risks of unexpected life events, leave many feeling unprepared for the financial demands of the present, let alone those of the future. Understanding these concerns, J Murry Financial stands as an ally to those seeking clarity and stability in their financial lives. As part of the Experior Financial Group family, J Murry Financial is equipped with innovative tools designed to demystify the complexities of financial planning. These resources are not just about numbers; they’re about providing a clear path forward for individuals and families who are striving to secure their financial well-being in an unpredictable world. At the heart of our approach is a commitment to personalized guidance. We recognize that each family’s financial situation is as unique as the dreams they harbor for the future. With the aid of Experior’s cutting-edge FiN and IPN tools, J Murry Financial agents are able to offer bespoke strategies that resonate with the individual needs and goals of our clients. It’s this tailored approach that enables families to approach their financial futures with renewed confidence and a sense of empowerment.

Empowerment through Experior’s FiN and IPN Tools

Navigating the journey to financial security can often feel like an attempt to solve a complex puzzle without all the pieces. This is where Experior’sFiN and IPN tools come into play, providing those vital missing pieces in the form of clear, actionable insights. The Financial Intelligence Number (FiN) is more than just a statistic; it’s a personalized guidepost that helps clients understand the amount of money they need to accumulate to enjoy a comfortable retirement without dependency on a paycheck. By considering individual lifestyles, financial goals, and the economic environment, the FiN tool aids J Murry Financial agents in outlining a clear and attainable retirement strategy for their clients. The Income Protection Number (IPN) complements the FiN by focusing on the present and ensuring clients’ immediate financial stability. It addresses a critical concern: the protection of a family’s income stream in the face of life’s uncertainties. The IPN tool helps clients gauge the amount of term life insurance coverage needed to safeguard their family’s financial future, should the unforeseen occur. With features that customize coverage and adapt to individual needs, the IPN tool simplifies the complex details of insurance policies, enabling clients to make informed decisions about protecting their income. By integrating these advanced tools into their practice, J Murry Financial agents are able to offer a comprehensive financial overview that resonates with the unique circumstances of each client. The FiN and IPN tools empower clients by demystifying the financial planning process, turning abstract numbers into a narrative that charts a path to financial freedom. This narrative is not just about reaching a destination but also about understanding the journey—identifying risks, exploring opportunities, and making adjustments as life evolves. In essence, the FiN and IPN tools are the embodiment of J Murry Financial’s client-centric philosophy. They serve as a testament to the agency’s dedication to empowering clients with knowledge, enabling them to take control of their financial futures with confidence. Through these tools, J Murry Financial agents are not just advisors; they are partners in their clients’ quest for financial well-being, providing guidance every step of the way.

Comprehensive Insurance Solutions for Every Need

We understand that life’s journey is filled with unexpected twists and turns. To help our clients navigate these uncertainties, we offer a diverse portfolio of insurance products, each designed to provide security and peace of mind for a variety of circumstances. Our offerings include term life insurance, which provides affordable coverage for a specified period, often with options for living benefits. These benefits can be a lifeline, offering financial support during the insured’s lifetime if they face a critical illness or chronic condition, thus ensuring that life’s unforeseen challenges do not compromise a family’s financial stability. For those seeking a more permanent solution, our permanent life insurance options, including whole and universal life policies, offer long-term coverage with the potential for cash value accumulation. This type of insurance is not just a safety net but an investment in the future, one that can play a pivotal role in a family’s financial planning. Additionally, to protect against the loss of income due to disability, our disability insurance products provide a reliable source of income, ensuring that our clients can maintain their quality of life even if they’re unable to work. Recognizing the increasing importance of managing long-term health conditions, we also provide critical illness and long-term care insurance. These policies offer financial support upon the diagnosis of a critical illness and coverage for care expenses in the event of a prolonged health issue, respectively. Such coverage is essential, as it addresses the significant costs associated with serious health challenges, which can otherwise deplete savings and investments intended for the future. At J Murry Financial, our advisors are skilled at helping clients select the right mix of insurance products to meet their unique needs. By taking the time to understand each client’s personal situation, goals, and concerns, we can tailor an insurance strategy that not only protects against immediate risks but also contributes to the achievement of long-term financial aspirations. It’s this thoughtful and thorough approach that sets us apart, ensuring that each client’s financial plan is as robust and resilient as the families we serve.

Experior’s Mission, Values, and Business Opportunity

At the core of Experior Financial Group’s operations lies a mission that resonates with the values and aspirations of J Murry Financial: to build robust financial foundations that not only empower families today but also pave the way for a lasting legacy. This mission is underpinned by a set of core values that serve as the compass guiding every interaction and decision. These values—service, giving, encouragement, leadership, teaching, and showing care & kindness—are more than mere words; they are the principles that shape the culture and define the client-focused approach of J Murry Financial. Service and giving form the bedrock of our community engagement, inspiring our agents to go beyond the call of duty to ensure the financial security and strategies that benefit the families and communities we serve. Encouragement and leadership are the driving forces behind our team’s efforts to provide accountable, ethical, and diligent guidance, fostering a nurturing environment where clients and agents alike can thrive. Through teaching, we impart financial literacy based on proven principles, equipping individuals and families with the knowledge to achieve personal financial freedom and responsibility. And in showing kindness, we embody compassion, respect, and generosity—listening, understanding, empathizing, and responding to the needs of those we serve. Beyond these values lies an exceptional business opportunity that Experior extends to its agents—a chance to embrace entrepreneurship and share in the company’s success. J Murry Financial agents have the unique prospect of gaining ownership stakes in their organization. This is achieved by reaching the executive director level, which includes building a team of licensed agents, thereby securing a lasting interest in the firm with a guaranteed buyout option for beneficiaries. Moreover, Experior’s innovative ownership model extends to offering company shares, reinforcing the belief that true opportunity includes providing a stake in the very company one helps to build. This distinctive model fosters a culture of shared growth and success, where every agent’s achievements contribute to the collective prosperity of the entire group. It’s a model that encourages collaboration, rewards initiative, and aligns personal advancement with the broader goals of the organization. As a result, J Murry Financial benefits from a team of motivated, invested professionals dedicated to delivering exceptional service and innovative financial solutions. Together, we are not just building a business but a community of shared values and shared success, where every family’s financial dream is within reach.

So What’s NEXT?

The journey to financial security is unique for each family, and the path is not always clear. That’s why J Murry Financial invites you to begin a conversation that could change the course of your financial future. By reaching out for a consultation, you take the first step towards a tailored financial plan that aligns with your aspirations and addresses your concerns. Our dedicated agents, equipped with Experior’s innovative FiN and IPN tools, are ready to help you navigate the complexities of retirement planning and income protection. The stories of those who have partnered with us are a testament to the transformative power of informed financial planning. Take the Thompson family, for instance, who, after a meticulous review of their financial situation through the FiN tool, discovered new strategies to enhance their retirement savings, ultimately securing a future they once thought was out of reach. Or consider the Rodriguez family, who, with the guidance of the IPN tool, now have peace of mind knowing their income is protected, and their children’s future is safeguarded, no matter what life may throw their way. These success stories are just a glimpse into the possibilities that unfold when you have a committed financial ally by your side. J Murry Financial is not just about providing insurance and financial services; it’s about building lasting relationships based on trust, empathy, and a shared vision for the future. We are driven by the belief that financial planning should be simple, accessible, understandable, and empowering, enabling you to make decisions with confidence. For those inspired by our mission and looking to create additional avenues of income, the Experior business opportunity offers a compelling path. As part of our team, you can achieve financial independence and help others do the same, all while building a stake in a growing organization that values your contribution and celebrates your success. We understand that taking the first step towards financial planning can be daunting, but with J Murry Financial, you’re not alone. Reach out to lead agent, Jason D Murry, today and let’s explore together how we can turn your financial goals into reality. Whether you’re seeking to fortify your family’s financial future or interested in the entrepreneurial opportunities within our dynamic team, your journey to financial empowerment starts here.

At J. Murry Financial, we understand the significance of being coachable when it comes to your financial well-being. Being coachable means being open to learning, adapting, and implementing valuable insights and strategies to achieve your financial goals. In this blog post, we’ll explore the importance of being coachable in financial planning and how it can benefit individuals across different life stages and financial situations.

Embracing New Perspectives: Being coachable in financial planning involves being open to new perspectives and ideas. Whether you’re a business owner, retiree, new investor, corporate executive, doctor, or start-up employee, being receptive to different financial strategies can lead to valuable insights that align with your unique financial aspirations.

Adapting to Changing Circumstances: Financial landscapes are constantly evolving, and being coachable allows individuals to adapt to changing circumstances. Whether it’s market fluctuations, tax law changes, or unexpected life events, a coachable mindset enables individuals to make informed decisions and adjustments to their financial plans.

Implementing Sound Advice: A coachable approach to financial planning involves implementing sound advice and recommendations from experienced professionals. Whether it’s portfolio management, tax strategy, legacy planning, risk management, or retirement strategy, being coachable allows individuals to benefit from the expertise of financial advisors and make informed decisions that align with their long-term financial goals.

Seeking Continuous Improvement: Being coachable in financial planning also means seeking continuous improvement and growth. It involves actively engaging in financial coaching, seeking educational resources, and staying informed about industry trends to make well-informed financial decisions that contribute to long-term financial success.

Building a Strong Financial Foundation: Ultimately, being coachable in financial planning is about building a strong financial foundation that aligns with your aspirations. Whether it’s wealth planning for high net worth individuals, managing debt and liabilities, or planning for future leadership, a coachable approach can lead to a robust financial strategy tailored to your specific needs.

In conclusion: being coachable in financial planning is essential for individuals across various life stages and financial situations. It involves embracing new perspectives, adapting to changing circumstances, implementing sound advice, seeking continuous improvement, and building a strong financial foundation. By adopting a coachable mindset, individuals can work towards achieving their financial aspirations with confidence and clarity.

If you’re ready to embrace a coachable approach to financial planning, reach out to me, Jason D. Murry, to start your journey towards financial success. Let’s work together to ensure that your financial plan remains adaptable, informed, and aligned with your unique financial goals.

As the lead professional associated with J. Murry Financial, I understand the importance of staying proactive and informed when it comes to your financial well-being. One crucial aspect of this is conducting an annual financial review to ensure that your financial plan remains aligned with your goals and aspirations.

Why an Annual Financial Review Matters: An annual financial review serves as a checkpoint to evaluate your current financial standing, reassess your goals, and make any necessary adjustments to your financial plan. It’s an opportunity to address any changes in your life, such as career advancements, family milestones, or unexpected financial challenges, and ensure that your financial strategy remains robust and effective.

Key Benefits of an Annual Financial Review:

Goal Alignment: By revisiting your financial goals annually, you can ensure that your investment strategies, retirement plans, and overall financial approach are in line with your evolving aspirations.

Risk Management: Identifying and mitigating potential risks, such as market fluctuations, changing tax laws, or unforeseen expenses, is crucial to maintaining financial stability.

Investment Performance: Evaluating the performance of your investment portfolio and making adjustments based on market trends and your risk tolerance can optimize your long-term financial growth.

Retirement Readiness: Assessing your retirement savings and income strategies annually can help you stay on track to achieve your retirement goals.

How J. Murry Financial Can Help: As a financial advisor with J. Murry Financial, I specialize in providing comprehensive financial reviews tailored to your specific needs and goals. Whether you’re a business owner, retiree, corporate executive, or medical professional, my expertise in wealth management, retirement strategy, and risk management can help ensure that your financial future remains secure.

The Annual Financial Review Process:

Personalized Consultation: I will conduct a thorough review of your financial situation, taking into account your current assets, liabilities, income, and expenses.

Goal Assessment: We will revisit your financial goals and aspirations to ensure that your investment and retirement strategies are aligned with your vision for the future.

Customized Recommendations: Based on our review, I will provide personalized recommendations to optimize your financial plan and address any areas of concern.

Ongoing Support: I am committed to providing ongoing support and guidance to help you navigate any changes in your financial landscape throughout the year.

Take the Next Step: Whether you’re a new investor, a seasoned business owner, or a retiree planning for the future, an annual financial review is a proactive step toward securing your financial well-being. Reach out to me,Jason D. Murry, to schedule your personalized annual financial review and take control of your financial future today.

Remember, proactive financial planning is the key to long-term financial success. Let’s work together to ensure that your financial plan remains robust, adaptable, and aligned with your aspirations.

Tax season is around the corner and it can be a stressful time for many individuals and businesses. However, with the right strategies in place, you can minimize your tax burden and maximize your savings. At J. Murry Financial, we specialize in helping our clients navigate the complex world of taxes and develop personalized strategies to save money. Let’s explore some expert tips for reducing your tax burden and keeping more of your hard-earned money. #TaxSavings #FinancialSuccess

Take Advantage of Tax-Advantaged Accounts:

One of the most effective ways to reduce your tax liability is by contributing to tax-advantaged accounts such as Individual Retirement Accounts (IRAs) or 401(k) plans. These accounts offer tax benefits, such as tax-deferred growth or tax-free withdrawals in retirement.

Maximize Deductions and Credits:

Deductions and credits can significantly reduce your taxable income. Be sure to take advantage of all available deductions, such as mortgage interest, student loan interest, and medical expenses. Additionally, explore tax credits, such as the Child Tax Credit or the Earned Income Tax Credit, which can directly reduce your tax liability.

Consider Charitable Contributions:

Donating to qualified charitable organizations not only supports causes you care about but can also provide tax benefits. By itemizing your deductions, you can deduct the value of your charitable contributions, potentially lowering your taxable income.

Plan for Capital Gains and Losses:

If you have investments, strategically managing your capital gains and losses can help reduce your tax liability. Consider selling investments with capital losses to offset capital gains and potentially lower your overall tax bill.

Consult with a Tax Professional:

Working with a knowledgeable tax professional can provide you with valuable insights and guidance tailored to your unique financial situation. They can help you navigate complex tax laws, identify potential deductions and credits, and ensure compliance with tax regulations.

Remember, tax planning is an ongoing process that requires regular review and adjustment. By staying informed about changes in tax laws and working with a trusted advisor, you can optimize your tax strategy and keep more of your money in your pocket.

Take the Next Step: Ready to maximize your savings and reduce your tax burden? Contact Jason D. Murry to schedule a consultation. Our team at J. Murry Financial is here to guide you through the intricacies of tax planning and help you develop a personalized strategy that aligns with your financial goals. Let’s work together to secure your financial success. #TaxPlanning #FinancialFreedom

Moving forward to tax season, don’t forget the key points we’ve discussed earlier: Taking advantage of Tax-Advantaged Accounts, Maximizing your Deductions and Credits, Consider Charitable Contributions to your church &/or other charitable organizations, Planning for Capital Gains & Losses, & most importantly, Contacting a tax professional.

Remember, at J. Murry Financial, we’re here to empower you with the knowledge and tools necessary to reduce your tax burden and maximize your savings. Contact us today to learn more about tax planning strategies and develop a personalized plan that aligns with your financial goals. Let’s work together to secure your financial success. #TaxSavings #FinancialSuccess

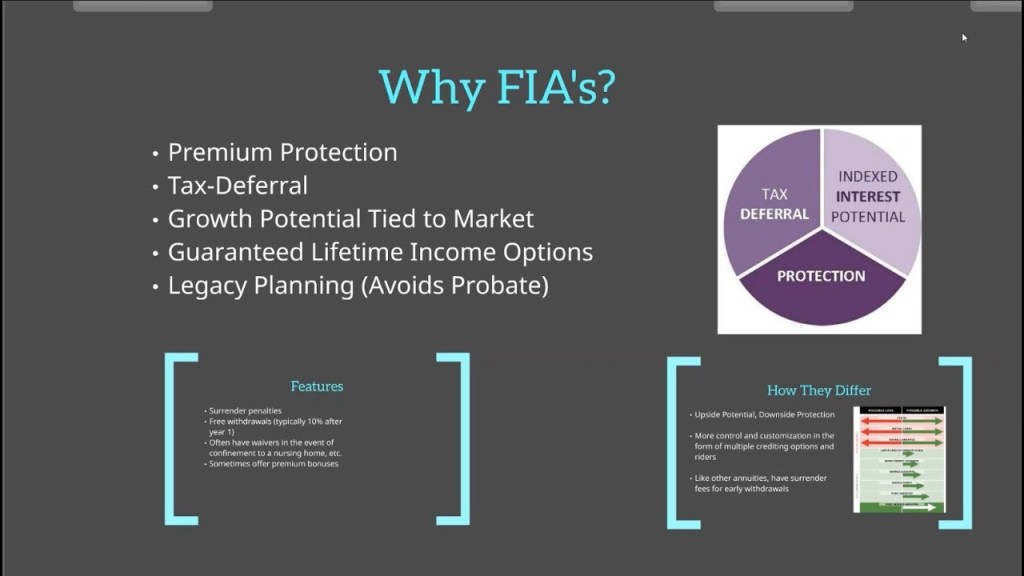

Are you looking for a reliable and secure way to grow your finances? Look no further than Fixed Index Annuities (FIA). At J. Murry Financial, we believe in empowering our clients with the knowledge and tools necessary to make informed financial decisions. In this article, we will explore the benefits of FIAs and how they can help you achieve your financial goals.

What are Fixed Index Annuities (FIA)? FIAs are insurance products that offer a unique combination of growth potential and downside protection. They provide you with the opportunity to participate in the potential growth of the stock market while protecting your principal from market downturns. This makes FIAs an attractive option for individuals who want to grow their money without the risk of losing it.

Benefits of Fixed Index Annuities:

Principal Protection: One of the key advantages of FIAs is that they offer protection for your principal investment. This means that even if the stock market experiences a downturn, your initial investment is safe.

Growth Potential:FIAs provide the opportunity to earn interest based on the performance of a specific stock market index, such as the S&P 500 & Russell 2000. This allows you to participate in market gains and potentially earn higher returns compared to traditional fixed-rate investments.

Tax-Deferred Growth: Another benefit of FIAs is that they offer tax-deferred growth. This means that you don’t have to pay taxes on the interest earned until you start withdrawing funds from the annuity. This can be advantageous for individuals looking to maximize their retirement savings.

Lifetime Income:FIAs can also provide you with a guaranteed stream of income for life. This can be especially beneficial for retirees who want to ensure a stable income during their golden years.

Flexibility:FIAs offer flexibility in terms of withdrawal options. Depending on the annuity contract, you may have the ability to make partial withdrawals or access your funds without penalty under certain circumstances.

Is a Fixed Index Annuity Right for You? While FIAs offer numerous benefits, it’s important to consider your individual financial goals and risk tolerance before making any investment decisions. At J. Murry Financial, we take a personalized approach to financial planning and can help you determine if an FIA genuinely aligns with your unique needs or to explore other options for your unique needs.

Take the Next Step: Ready to explore the benefits of FIAs and unlock your financial growth? Contact Jason D. Murry to schedule a free consultation. Our team of experts is dedicated to helping you achieve your financial goals and providing you with the knowledge and support you need along the way. Together, let’s pave the path to a brighter financial future. #FinancialGrowth #Empowerment #FIAincome #Assets #Investing

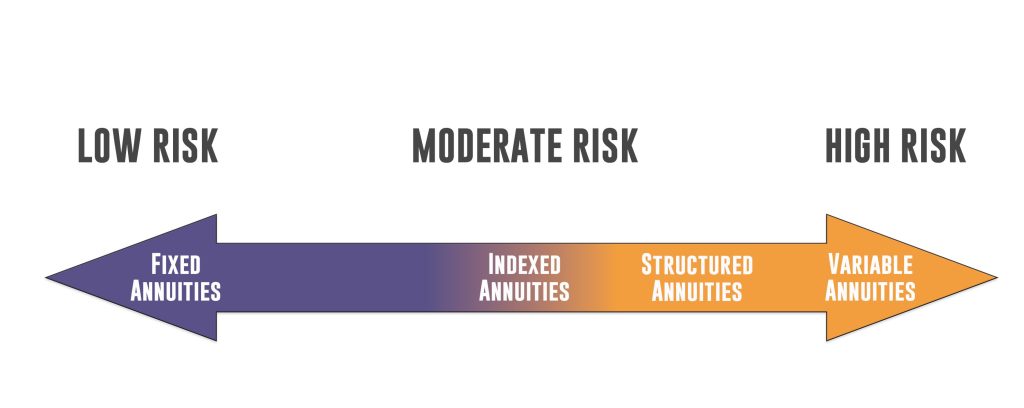

Again, FIAs are mid-risk investments primarily benefit the clients who desire to Protect their Initial Premiums, have Growth Potential through Stock Market Indices such as; the S&P 500 and Russell 2000, Tax-Deferred Growth, Lifetime Income, Flexible Withdrawals, & to Avoid Probate.

Remember, at J. Murry Financial, we’re here to guide you on your financial journey and help you make informed decisions. Contact us today to learn more about the benefits of FIAs and how they can support your financial goals. Let’s work together to unlock your full financial potential. #FinancialSuccess #Empowerment

Introduction: Are you tired of being burdened by debt and longing for financial freedom? Look no further than J. Murry Financial, led by professionals like Jason D. Murry. With our comprehensive range of services and expertise in managing debt and liabilities, we can help you eliminate debt and pave the way to a brighter financial future.

Core Competencies and Tailored Solutions: At J. Murry Financial, we understand the stress and challenges that come with debt. That’s why we offer personalized debt elimination strategies tailored to your unique financial situation. Our core competencies include debt management, budgeting, and financial coaching, all aimed at helping you regain control of your finances.

Customized Debt Elimination Plan: Our team of experts will work closely with you to create a customized plan that fits your needs and goals. We’ll analyze your current debt, assess your income and expenses, and develop a strategy to pay off your debts efficiently. With our guidance, you’ll learn effective budgeting techniques and smart financial habits that will set you on the path to long-term financial success.

Building a Solid Financial Foundation: At J. Murry Financial, we believe that financial freedom is within reach for everyone. Our services go beyond debt elimination – we empower you to build a solid financial foundation for the future. Whether you’re a business owner, retiree, or start-up employee, our comprehensive solutions will help you achieve your financial goals.

Take the First Step: Don’t let debt hold you back any longer. Take the first step towards financial freedom by (1) Unlocking your FiN: https://discoverfin.io/en?id=finjas22oq (2) Scheduling your Free Consultation with Jason D. Murry: https://card.discoverfin.io/finjas22oq_personal. Let J. Murry Financial be your partner in eliminating debt and building a brighter financial future. #DebtElimination #FinancialFreedom #JMurryFinancial #UnlockYourFiN